The problem with budgeting systems is that they tend to be either overly meticulous, leaving little room for flexibility, or too simplistic, failing to break down spending categories sufficiently. The former requires a tremendous amount of time to implement and oversee. Therefore, it is eventually abandoned as it proves too complex. The latter leaves large amounts of unknown expenditures. Both fail to account for the number of variables that make real-time decisions possible.

Alternatively, an effective system will, at most, give you the tools to make good decisions in the moment so those choices keep your future goals on-track. At least, a successful system should allow you to see where your spending priorities lie.

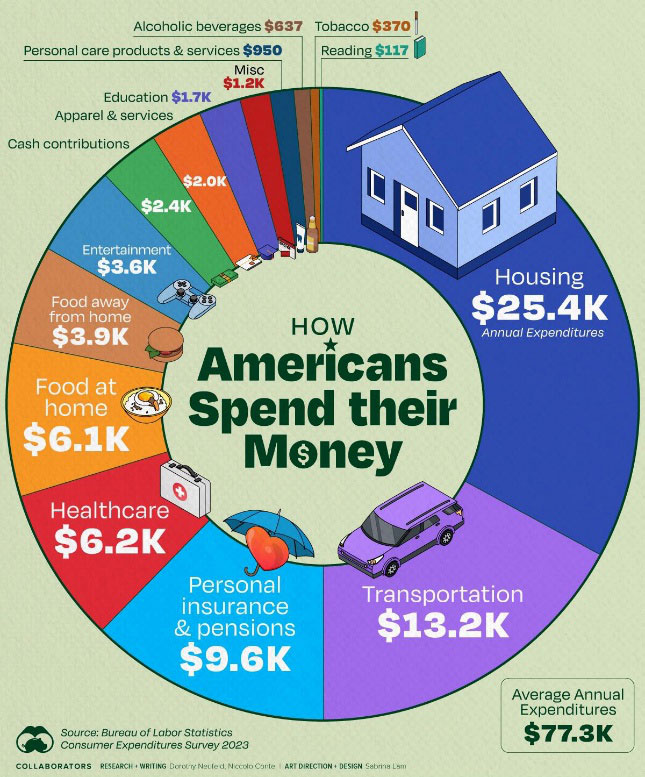

At the end of the day, our choices on what we do with our money fall into three buckets; 1) Past decisions, 2) Present decisions, 3) Future decisions. We spend a fixed, reoccurring amount of money today for items agreed upon in the past. We maintain a present, day-to-day lifestyle involving variable one-time dollar outlays. Lastly, we all have future goals that necessitate savings for tomorrow.

Each of these three buckets need to be comprised of their own separate bank account. First, figure out how much money is needed each month to fund your future goals and have that amount direct deposited from your paycheck into your savings account if you haven’t established an emergency fund or an investment account otherwise. Examples of expenditures that will come from this account include vacations, home improvements, car replacement, health insurance deductibles and education funding.

The remaining portion of your net pay is direct deposited into a checking account we’ll call your fixed account. It is critical to know how much it costs to operate your household for one month. Once this amount is determined, all of your known fixed expenses will come from this checking account. Common items include mortgage/rent, car payment, insurance, property taxes and utilities. The most efficient way is to set-up an automatic bill payment on-line.

Next, establish a second checking account referred to as your variable account. Figure out your monthly discretionary expenses and set up an automatic transfer of half of that amount twice a month from your fixed account to your variable account (you can even do it weekly if you would like). You will use your debit card to pay for things such as groceries, clothes, entertainment, recreation, home furnishings, consumer purchases and dining out. If you don’t currently know your budget for all of your variable expenses, it may take a few months to find the right dollar amount for you.

It is not necessary to transfer the entire surplus from your fixed account into your variable account to spend each month. An optional method is to let some of the surplus from your fixed account accumulate for a later transfer into savings or create a monthly bank draft into a taxable investment account. After all, some of the fixed expenses are annual and you may need a small cushion.

Separating your money into buckets works on many levels as it is simple to implement and follow:

- Encourages a debt-free approach to life.

- No need to track expenses. All that is needed is to watch your balance on your variable checking account.

- Creates an incentive to save. Not only are future goals rewarded, but money left over in your variable account can be spent guilt-free on discretionary items.

- Creates an artificial scarcity that allows you to prioritize your spending habits.

- Promotes flexibility of choices as specific categories are not established.

- It will create clear spending boundaries by preventing the need for credit cards.

- You’ll know where you stand at all times, not just at the end of the month, quarter, etc.

- Married couples are now on the same page financially. Although priorities differ, but spending amounts are agreed upon and funded ahead of time so the items cost is irrelevant.

- Promotes a balanced lifestyle by not letting one bucket, i.e. high fixed expenses, create a shortage in your current lifestyle thereby decreasing the likelihood of accumulating future debt.

- Most importantly, it allows you to make better decisions today that will broaden your future options tomorrow. For example, you may rethink your ability to afford a new car payment as your monthly variable account has to be reduced to offset the increase in the fixed account. Therefore, you may opt to settle for paying cash for a used car from your savings.

The benefits are numerous…ensuring there is money for the ‘needs’ in life and money spent on the wants’ in life are what you truly desired.

There are many variations to this approach to your finances, so be creative and customize this system to fit your individual and unique situation. Get organized and regain control of your financial life today!